7th July - A Muted Re-Open

- Jul 7

- 5 min read

Yesterday saw the markets reopen after the long weekend, but not a lot happened. After the Independence Day closure of the markets on Friday, markets reopened on Monday after a weekend of celebration in the US and a weekend of mourning in Iran. Talks between the two will not resume until the 11th of July, so the Middle East situation did not provide any news for the markets to get their teeth into.

Markets are currently fixed on next week's CPI print, which will be the first inflation reading to take into account the reduction in oil prices back down to pre-war levels. This will be the first real indication of how sticky inflation will be. Has the energy shock baked in prices for the longer run, or will prices fall back to previous levels quickly now that oil is no longer at $120 a barrel? The outcome will have a key impact on the FOMC's interest rate decisions and so will have a huge effect on all markets. It is gearing up to be the largest news release of the summer.

Forex

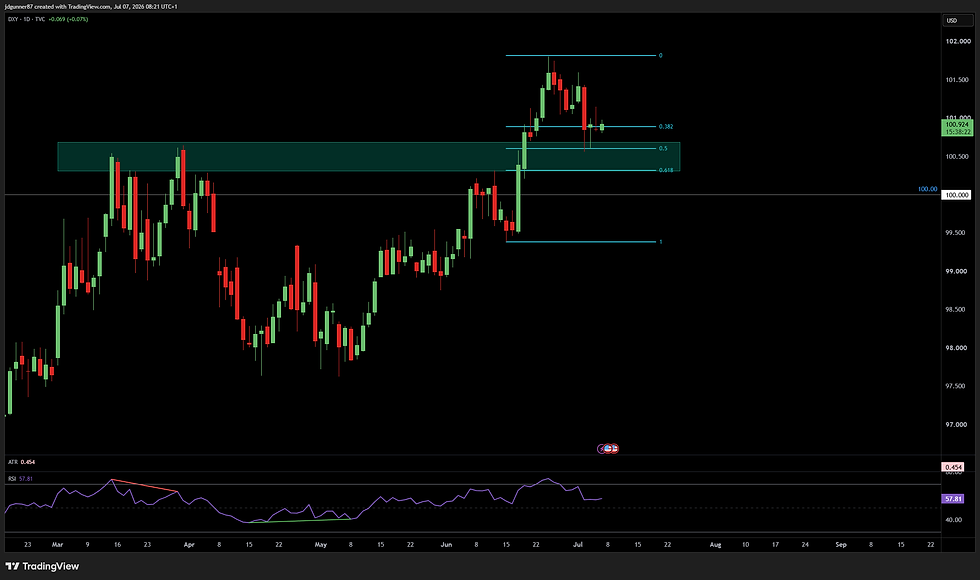

The USD remained on the back foot yesterday despite trying to rally higher, pressured by treasury yields drifting lower and still struggling against the headwind of weak NFP prints last week. As September hikes are now seemingly off the table, the USD has lost the reason for its strength over the past few weeks and is slowly drifting back towards the 100.000 level. The technical setup does still seem strong though, as we have recently broken through a level that had been providing resistance for over a year and are only now coming back to re-test it. A hot CPI print next week could easily throw fuel back onto the USD fire and see it push further north, but at present the market seems to be waiting and watching.

The USD/JPY is, once again, pushing back up towards recent highs, having seen a likely intervention before NFP last Thursday. The speed of the recovery has been impressive, recovering almost all of the pair's losses in just 2 days as the JPY struggles in a risk-on environment. Having thought they may have bought themselves some time, the BoJ is now once again faced with the choice to intervene or allow the market to play out. We also, once again, have a looming economic print on the horizon in next week's CPI, so the BoJ could do as it did last week and wait until CPI day to act. This pair seems to be in a continuous cycle of intervention and recovery; there will need to be something significant to break us out of this loop.

The GBP continued to show strength yesterday, as the market grows increasingly comfortable in the belief that there will be an orderly transition from one Prime Minister to the next, with the GBP gaining on Monday against all other major currencies. The EUR was mixed on the day, whilst the CHF struggled in the same way that JPY did, with both safe-haven currencies feeling the force of a risk-on day. CAD continues to be weighed down by lower oil prices, whilst the AUD and NZD enjoyed the fruits of a risk-on day and the bounce in precious metals. The risk-on environment may only really play out at the start of this week, as we can expect to see some risk mitigation over the coming days as investors prepare for CPI next week and any unexpected surprises this may bring.

Indices

The major indices had a positive start to the week, with American, Japanese & British indices all broadly positive on the day. The Dow continues to outperform the more tech-heavy indices, making yet another end-of-day all-time high yesterday at over 53,000 and up 0.4% on the day. The S&P was also up 0.4% on the day, whilst the Nasdaq was level at the close. It is worth noting that the Nasdaq had a 1.5% swing between the high and the low on the day, implying there was some minor volatility there. It seems the AI/tech sector is still choppy and has not yet settled on a clear direction, something that is backed up when you look at the Nasdaq as a whole for the last few weeks. The fact that this is choppy whilst the Dow continues to move higher could be another indication that we are seeing the slow movement from growth to value, as has been noted a number of times on this blog.

It will be very interesting to see how the CPI print next week affects indices. We may see some form of small pullback as investors protect their capital before then, before they pick a direction post-CPI and we see some significant moves. Next week could be key for the AI/tech balloon's health.

Precious Metals

Both Gold and Silver pulled back a little yesterday, with Gold down 0.35% and Silver down 1.35%. The risk-on sentiment in the market overall will have hurt metals on the day, but the real question is whether this is a sign that the recent gains from metals were a 'dead cat bounce' or whether it was the start of a longer-term recovery in metals prices.

For Gold, the bounce has come at a significant technical level of $4000 and was supported by the NFP figures on Thursday. We are now, though, coming back up to hit a two-month-long trend line, as well as testing the $4200 level. As a result, the technical side is no longer seeing a case for Gold to move higher. On top of this, the medium-term prediction is for US rate hikes before the end of the year (now predicted to be in October), so there may still be some downside before we see a longer-term recovery. I would expect to see further moves lower for metals over the coming weeks and months until we reach the end of this rate-hike cycle, before prices begin to recover once the FOMC indicates an intention to begin lowering interest rates back down.

The key CPI print next week therefore takes on huge significance for metals. If we see a very soft print, it could remove rate hikes from the picture entirely, and metals will see huge support. A hot print could move rate hikes up and keep them there for longer, which would be a huge negative for metals. Next week, therefore, is key.

Today's Market Drivers

RBNZ Interest Rate Statement, 3 a.m. Wed morning, UK time - The only significant data release over the next 24 hours will be the interest rate decision from New Zealand. Last time we saw unexpectedly hawkish comments from the RBNZ, so this month the commentary will be keenly analyzed.

Pre-CPI Positioning - Apart from the RBNZ statement, there is no real other news to announce, so markets will most likely be focusing on next week and moving their capital around in advance of the release.

Comments