29th May - Deal Agreed?

- May 29

- 5 min read

Geopolitics

Yesterday was a perfect illustration of the contradictions we have seen over the past few weeks - genuine diplomatic progress and military escalation within the same 24 hours.

News broke yesterday that a tentative deal had been agreed to extend the ceasefire by 60 days and to launch talks on Iran's nuclear program. This is now with President Trump, who has not yet signed off on the deal, noting that he would like a few days to think about it. It has also been noted that Supreme Leader Khamenei has not yet signed off on the 'Memorandum Of Understanding' either, while Iran has said that the text of the MOU has not yet been finalized. This is a breakthrough, but maybe not as complete as had been originally considered. Vice President Vance commented on the deal, saying the deal was "very close," but that the two sides were "going back and forth on a couple of language points."

However, we then saw confirmation from the US overnight that the Iranians had fired a ballistic missile towards Kuwait, which had been intercepted before hitting its target. This is the first time in this phase of the conflict that Iran has directly attacked a Gulf neighbour and is a potential widening of the conflict. It was immediately condemned by the UAE, Saudi Arabia, and Qatar.

This is another example of what seems to be a disconnect between Iran's negotiators and its military, which creates a problem for markets. Do they focus on the deal or the attacks? The fact that Trump has taken time to consider the agreement implies the US is not completely happy with the deal, also implying that the military action is a genuine obstacle and not just noise.

Forex

Yesterday's price action for the USD was a tale of two halves. Through the morning in Europe, the USD was gaining ground after the escalation on Wednesday. The gains then began to pare back and were completely reversed once the deal was announced. The DXY ended the day close to 99.000, 0.3% down on the day and 0.55% down on the intraday high.

EUR/USD and GBP/USD followed this pattern, with both falling overnight before pulling back to finish the day positive, with the EUR/USD ending the day up 0.2% and the GBP/USD up 0.13%. The EUR outperformed the GBP slightly, due to the shifting of ECB expectations towards rate hikes giving it a larger base of support, whilst the continued political uncertainty in the UK dampened demand for the GBP. Both pairs, however, were mainly driven by USD weakness on the day. One thing to note, the peace deal announcement only accounted for half of the USD's move on the day, when such an announcement would normally cause a huge move in the market. The implication is that a peace deal being agreed has already been largely priced in with the USD. This matters for two reasons, the first being that any negative news on the deal will therefore have far more of an impact than any further positive news, creating an asymmetric risk with USD. Secondly, it may mean that markets are now more sensitive to economic data releases than when the war was at its peak. If markets are already pricing in an end to the war, they will then revert back to normal economic data for forward indicators. This brings back the importance of things such as yesterday's US Core PCE and US GDP figures, both of which were lower than expected and added to the push lower in USD.

In terms of commodity currencies, the AUD had a positive day as we saw a rise in precious metal prices, whilst the CAD struggled somewhat on lower oil prices. The main story, however, continued to be NZD, which continued to be supported by a wave of strength in the wake of the RBNZ's comments earlier in the week. The AUD/NZD has fallen a huge 2.2% since the RBNZ's decision, and may yet fall further as the market continues to digest the information. If we see some profit-taking in NZD and a pullback in the market, it could be an excellent time for a trade to back further NZD strength.

Indices

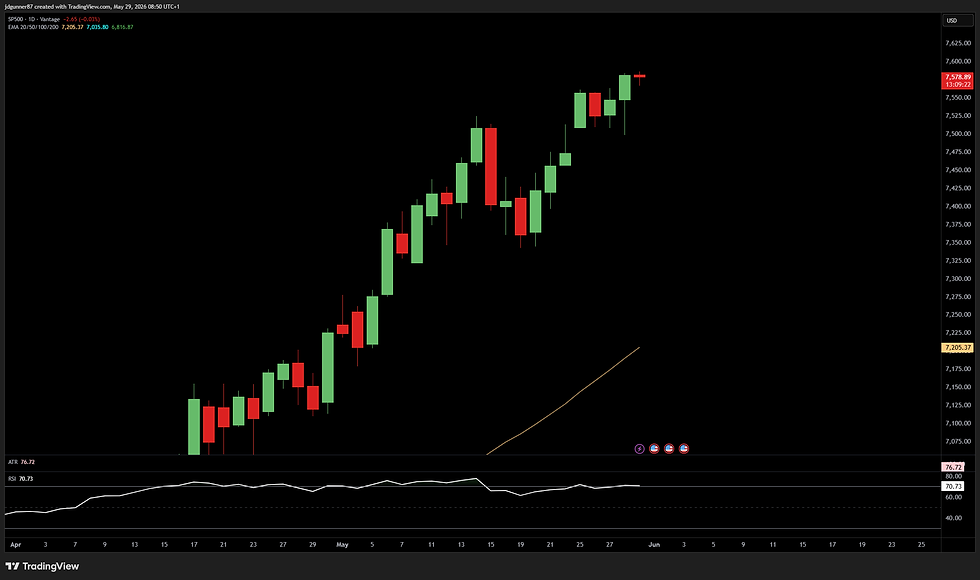

The S&P 500 and Nasdaq both made new close-of-day highs yesterday, boosted by better-than-expected PCE figures and the peace deal news from Iran. They also seem to have largely ignored the fact that while better than expected, the PCE figure was still the highest it has been in 3 years, as well as discounting the strikes by Iran in Kuwait. Markets are still very much in 'deal guaranteed' mode and are assuming that any uncertainty around the US-Iran agreement is nothing more than posturing and part of negotiations. This may well be the case, and we may see a deal agreed and signed over the coming days. It does leave the market at significant risk, however, if a deal is not agreed or if there is further meaningful escalation. To reiterate previous statements made on this blog with regards to indices, in the short term there is likely more to lose than there is to gain if you go long in today's market.

Precious Metals

Both Gold and Silver steadied after falling through the week, backed by the news from the Middle East as well as a better-than-expected PCE number. This move up would not have been caused by any change in safe-haven demand, but instead by lowering expectations of rate hikes caused by the better-than-expected PCE figure. Added to this, the potential deal increases the possibility of the Strait of Hormuz reopening and oil prices falling, again reducing inflation concerns and lowering interest rate predictions. The future for Gold in particular will now depend on how quickly inflation falls if a deal is reached, then how interest rate expectations change based on this. If inflation is now baked into the economy for the near future as is feared, we could see Gold struggle for the remainder of the year.

Silver also saw support yesterday for the same reasons. As has been mentioned in past posts, Silver's industrial applications in the tech world give it a stronger base in my opinion, meaning it is less likely to have a sustained drop in price in the long run. The short-term pricing, however, will depend on news from Iran and how that shapes inflation expectations.

Today's Key Market Drivers

Iran Peace Deal - Any updates on the deal will move the market and remains the most significant catalyst for near-term price action.

BOE Gov Bailey Speaks - This could be a market mover for GBP if there are any unexpected comments or changes in stance from the BOE moving forward.

CAD GDP, 1:30 pm UK time - This will show us how the Canadian economy is holding up amid the energy shock, giving guidance to future performance and may affect how the BoC acts in future months.

Comments