1st July - From Oil Deficit To Surplus?

- Jul 1

- 3 min read

The ceasefire continues to hold, and oil is now flowing through the Strait of Hormuz. Talks between the US and Iran are still grinding along slowly, but they are still struggling with the same issues as before. The key development from yesterday was that analysts are beginning to believe that we may be moving towards an oil surplus rather than a deficit. With the oil supplies that had been stagnant in the Strait during the war now released, all of that supply will hit the market at the same time. Coupled with weakening Chinese demand, this may lead to too much oil available instead of not enough.

The consequence of this would be oil prices lowering further and more disinflationary pressure, meaning the FOMC's hawkish dot-plot from last month may not end up being needed.

Forex

The USD was mixed on the day, as markets continue to wait for the NFP report due to be released tomorrow. Yesterday we saw a strong JOLTS jobs number but a weaker CB Consumer Confidence print, which seemed to counteract each other and leave the USD close to where it opened at the end of the day. Normally, we would expect JOLTS to have more of an effect than consumer confidence, which makes the lack of movement outside of the noise around the event interesting. This could be a sign that the hawkish dot-plot is now fully priced in, but it could also just mean that capital is waiting for the NFP print before deciding on a direction to target.

The most interesting pair is still the USD/JPY, which has continued to rise past recent intervention levels and is now at the highest level since 1986. The BoJ is now under serious pressure if it is to continue to defend the JPY's position. My feeling is that this may come to a head at the release of the NFP figures tomorrow. A weak report for the USD will move the pair in the JPY's favor and the BoJ may not have to intervene; a stronger print and the BoJ may decide that they cannot wait any longer. That is, of course, if they still want to intervene at all.

Outside of the USD, the JPY and CHF continued to show weakness as the safe-haven flows moved away from the two currencies, while the EUR, CAD, and GBP had mixed days. The AUD and NZD, however, had very positive days yesterday, boosted by the moves towards risk-on markets in general. It is worth noting, as is the case with all currencies, that yesterday's price action was muddled by end-of-quarter movements. There is every chance that a positive or negative day is not indicative of future movement and was just noise as institutions adjusted their exposures. We would need to see a longer trend into July before making any longer-term calls.

Indices

Yesterday saw a second successive positive day for all US indices, with technology being a particularly strong performer. The day capped the best quarter for the major US indices since the pandemic in 2020, thanks to the astonishing rally following the initial Iran war dip.

As with the forex pairs, some of this would have been end-of-quarter positioning, but there is still value in analyzing the moves of the day. The mega-cap tech stocks had a good day, but we also saw a positive day for non-tech stocks as well. As of Monday, 64% of S&P 500 stocks traded above their 50-day moving average, up from just 50% a month ago, even though the S&P posted a loss for the month overall. The implication seems to be that we are indeed moving into a less concentrated market and moving away from focusing on only a small number of huge companies. The balloon may yet be deflating slowly rather than filling with more air ready to pop.

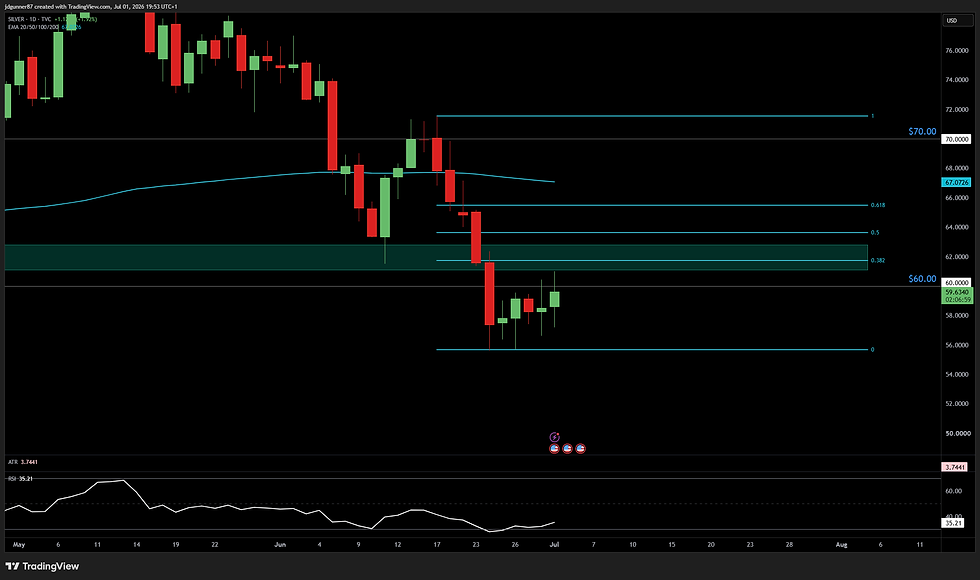

Precious Metals

Gold and silver were relatively flat yesterday in the end, despite some noise during the day. Both seem to be in a similar situation to the rest of the markets, in that they are waiting to see what happens with NFP before markets decide on a short-term direction for the metals. Tomorrow could be key for the metals' performance for the rest of 2026.

Today's Market Drivers

USD ISM Manufacturing PMI, 3pm UK time - This will be another warmup for the NFP figures tomorrow; markets may only react to a really unexpected number.

Fed Chair Warsh & BoE Gov Bailey Speak - Both heads of central banks will be speaking today, so any unexpected remarks will be taken into consideration.

Q3 & pre-NFP positioning - There could be some noise in the markets today as institutions prepare themselves both for the start of Q3 and for NFP tomorrow.

Comments